Detailed Analysis of Joint Order No. 0043/AC/MINDDEVEL/MINFI of 15 May 2026 (Local Tax Monitoring Units)

- Summary of the Law- The big picture

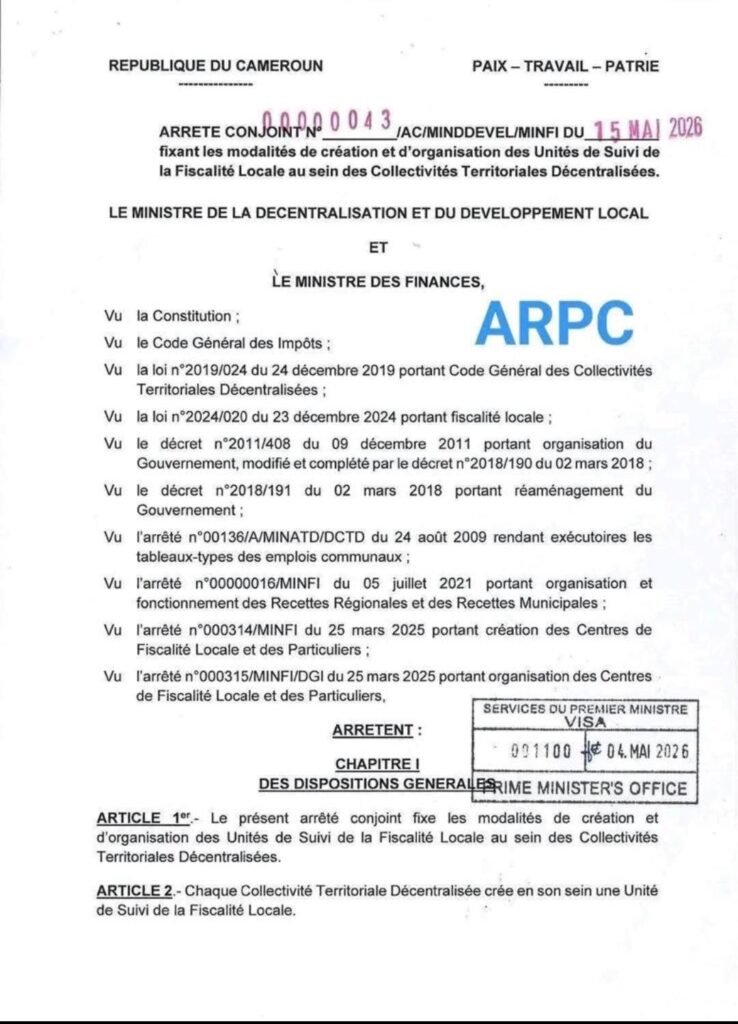

On May 15, 2026, Ministers Louis Paul Motaze (Finance) and Georges Elanga Obam (Decentralization) signed Joint Order No. 0043/AC/MINDDEVEL/MINFI. On the surface, it creates “Local Tax Monitoring Units” (LTMUs) within Cameroon’s communes and regions. But buried in the fine print is a seismic shift.

This Joint Order, mandates that every decentralized local authority (Communes, Urban Communities, Arrondissement Communes, and Regions) must create a “Unité de Suivi de la Fiscalité Locale” (Local Tax Monitoring Unit – LTMU) .

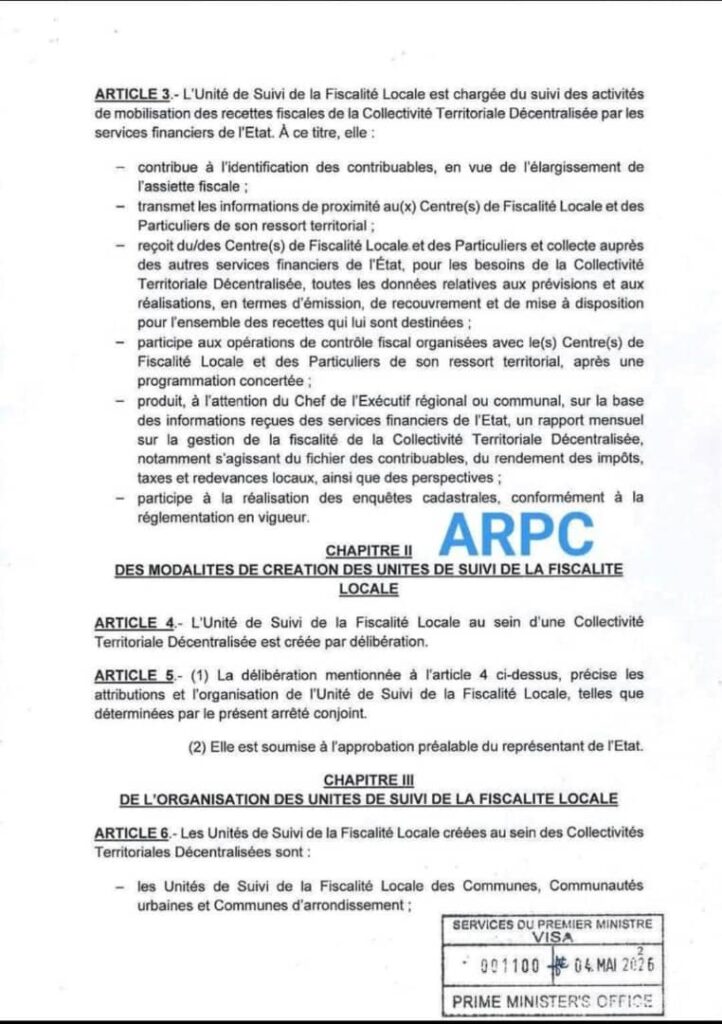

The LTMU is not a tax collection body but a local oversight and liaison unit. Its core functions are:

- Identify local taxpayers to broaden the tax base.

- Transmit local intelligence to State-run “Local Tax and Individual Centers.”

- Collect and centralize data from State financial services on tax forecasts, actual issuance, recovery, and transfer of local revenues.

- Participate in joint tax audits with State centers after coordinated planning.

- Produce a monthly fiscal report for the local executive (Mayor or Regional President), covering taxpayer files, local tax performance, and outlook.

- Assist in cadastral surveys (property mapping).

Creation process: Each Local Council must pass a deliberation (local law) to create its LTMU, but this deliberation requires prior approval by the State’s local representative (the Senior Divisional Officer or Governor). The Order sets the general framework, while local deliberations specify internal organization.

Article 13 of the accompanying legal framework states unequivocally:

“Budget authorities and accountants of Communes, Arrondissement Communes, and Urban Communities are hereby divested, each concerning their respective responsibilities, of their prerogatives relating to the issuance of tax revenues and the recovery of communal taxes, duties, and fees.”

Let that sink in. Mayors and local treasurers no longer have the legal right to issue or collect their own taxes. The State has effectively re-centralized local fiscal power.

WHAT REPLACES THE MAYORS’ POWER?

Local authorities now get Local Tax Monitoring Units (LTMUs) – not collection agencies, but oversight and liaison bodies. Their job:

- Identify taxpayers

- Share local intelligence with State tax centers (DGI)

- Collect performance data from State services

- Participate in joint audits

- Produce monthly reports for the local executive

- Assist in cadastral surveys

Critical catch: Even creating an LTMU requires a local deliberation that must be pre-approved by the State’s local representative (Governor or Senior Divisional Officer). No approval = no unit.

WHY THIS MATTERS FOR DECENTRALIZATION

Cameroon’s 1996 Constitution and the 2019 General Code of Decentralized Territorial Authorities promised genuine local autonomy. This Order does the opposite:

| Aspect | Before (Theoretical) | Now (Actual) |

| Tax issuance power | Mayors & local accountants | State tax services (DGI) |

| Tax collection power | Local receivers | State collectors |

| Local role | Active management | Passive monitoring & reporting |

| State control | Indirect via supervision | Direct via veto over LTMU creation |

This is administrative re-centralization dressed as technical support.

STRENGTHS (From the State’s perspective)

✅ Better tax intelligence – Local units feed real-world data to DGI

✅ Reduces informal collection – Ends opaque contracts with private “receivers” for advertising fees, etc.

✅ Uniform enforcement – National standards replace fragmented local practices

✅ Fights tax evasion – Combined cadastral surveys + local knowledge

WEAKNESSES (For local democracy & citizens)

❌ Unfunded mandate – No budget, staff, or resources provided for LTMUs

❌ No local coercive power – Mayors can monitor but cannot compel payment

❌ State veto on creation – A hostile local State representative can block any LTMU

❌ Risk of double harassment – Citizens may face both State agents and local “monitors”

❌ Kills fiscal accountability – If locals don’t collect, they can’t be held responsible for poor service delivery

❌ Contradicts decentralization – Centralizes what should be local

PRACTICAL IMPACT ON THE GROUND

For the State: Low-risk way to increase tax compliance without sharing power. But creates bureaucratic duplication and potential friction between DGI agents and local monitors.

For citizens: Unclear benefit. If the State collects more but does not transfer more to communes, citizens see no improvement. Worse – they face more enforcement without better services.

For mayors & councils: Become fiscal informants, not fiscal managers. Monthly reports to the executive are useful, but without action power, they are toothless watchdogs.

For private advertising receivers & third-party collectors: Many contracts for urban advertising fees, concession revenues, and other local levies are now legally void. Expect litigation.

THE REAL QUESTION: IS THIS A BETTER OPTION?

Compared to the old chaotic system (where some communes had no collection capacity, others outsourced to unregulated private agents), yes – this creates a single, state-run framework.

But compared to genuine decentralization? No. True local autonomy requires local assessment, collection, and enforcement, with national standards and oversight – not complete State takeover.

This Order is a technocratic half-step: transparency without power, data without decision-making.

WHAT SHOULD HAPPEN NEXT

If the government is serious about local development, it must:

- Fund LTMUs properly – e.g., 1% of locally collected revenues automatically allocated

- Remove the prior State approval clause – Make LTMU creation automatic once the law is published

- Guarantee data sharing – Mandate monthly transfer of all local tax data from DGI to councils

- Pilot co-collection – Allow high-performing communes to regain collection rights under State supervision

- Publish revenue transfer reports – Citizens must see whether more local tax actually reaches local budgets

FINAL VERDICT

This reform solves one problem (fragmented, opaque local tax collection) but creates a bigger one (eroding local fiscal autonomy). Cameroon’s decentralization is now officially fiscal follow-up without fiscal power.

For advocates of local democracy, this is a setback. For centralists, it’s a logical consolidation. For the average citizen – wait and see whether their roads, schools, and clinics improve. If not, the only thing that changed is who holds the receipt book.

Let’s discuss. Does this strengthen or weaken Cameroon’s decentralization? Drop your thoughts below.

#Cameroon #Decentralization #LocalTaxation #FiscalReform #MINFI #MINDDEVEL #DGI #LocalGovernance #TaxPolicy #PublicFinance #AdministrativeLaw #Communes #Mayors #CEMAC #GovernanceReform