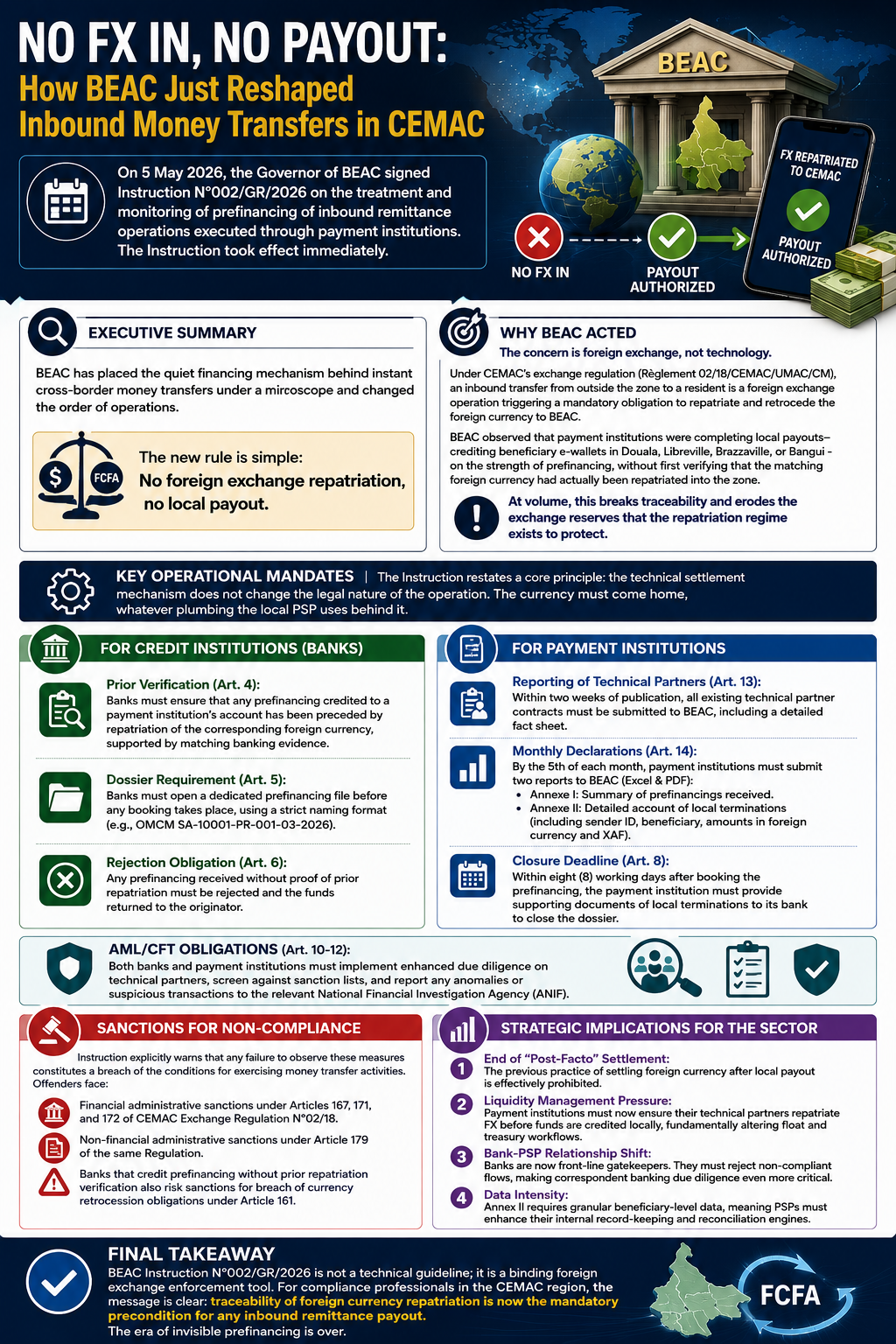

NO FX IN, NO PAYOUT: How BEAC Just Reshaped Inbound Money Transfers in CEMAC

Executive Summary

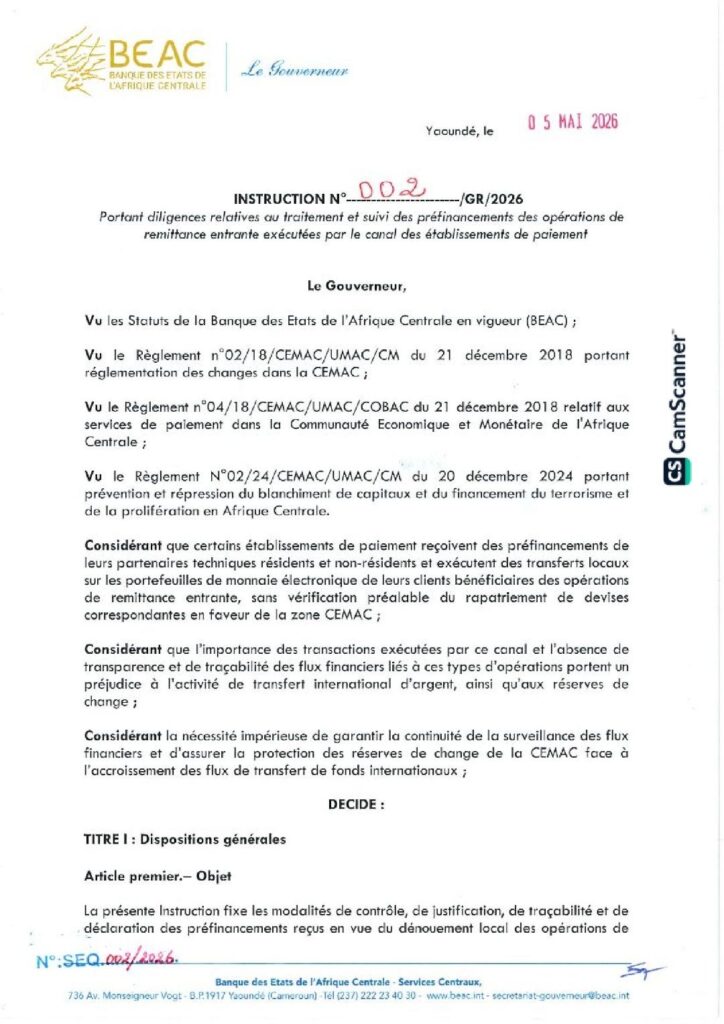

On 5 May 2026, the Governor of the Bank of Central African States (BEAC) signed Instruction N°002/GR/2026 on the treatment and monitoring of prefinancing of inbound remittance operations executed through payment institutions. The Instruction took effect immediately upon signature.

In plain terms, BEAC has placed the quiet financing mechanism behind instant cross-border money transfers under a microscope and changed the order of operations. The new rule is simple: No foreign exchange repatriation, no local payout.

Why BEAC Acted

The concern is foreign exchange, not technology.

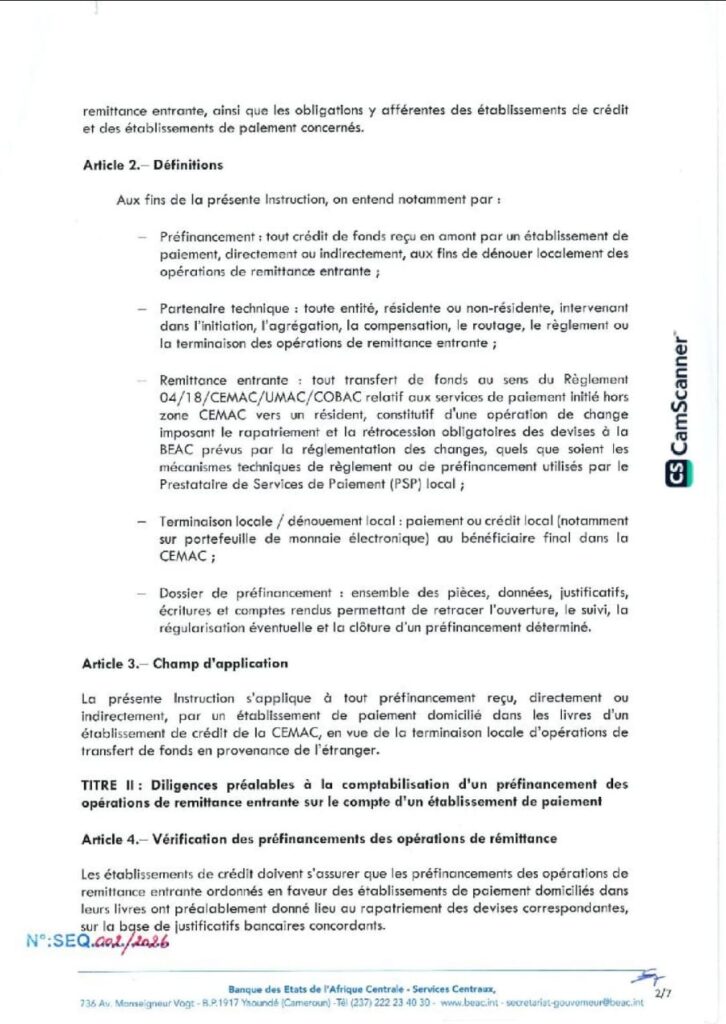

Under CEMAC’s exchange regulation (Règlement 02/18/CEMAC/UMAC/CM), an inbound transfer from outside the zone to a resident is a foreign exchange operation triggering a mandatory obligation to repatriate and retrocede the foreign currency to BEAC.

BEAC observed that payment institutions were completing local payouts—crediting beneficiary e-wallets in Douala, Libreville, Brazzaville, or Bangui – on the strength of prefinancing, without first verifying that the matching foreign currency had actually been repatriated into the zone.

At volume, this breaks traceability and erodes the exchange reserves that the repatriation regime exists to protect.

Key Operational Mandates

The Instruction restates a core principle: the technical settlement mechanism does not change the legal nature of the operation. The currency must come home, whatever plumbing the local PSP uses behind it.

For Credit Institutions (Banks):

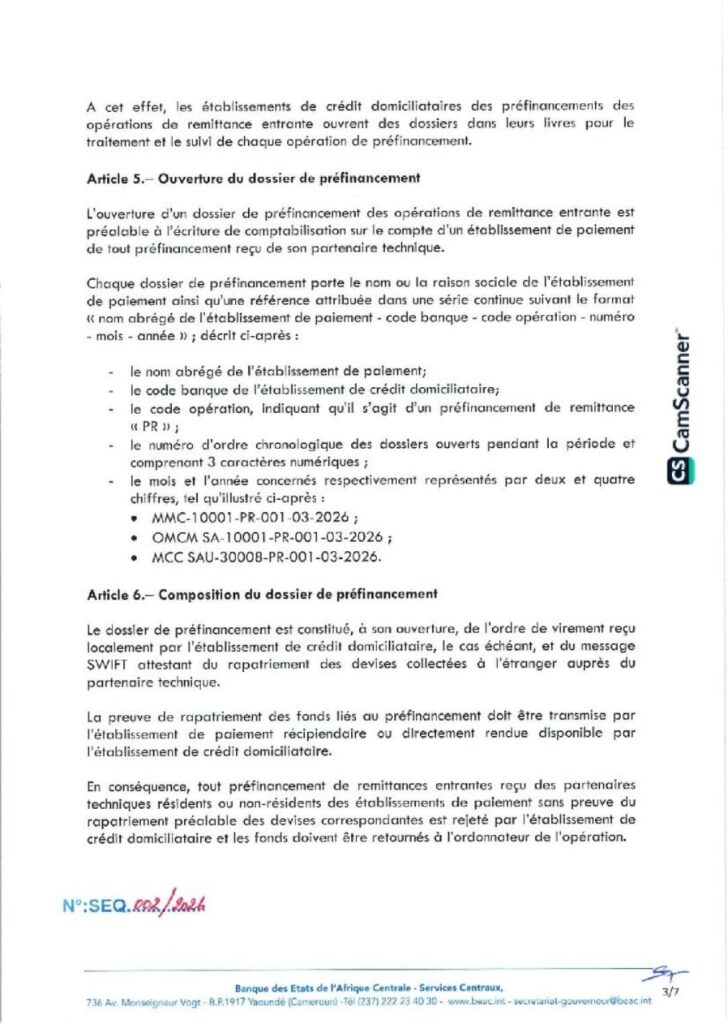

- Prior Verification (Art. 4): Banks must ensure that any prefinancing credited to a payment institution’s account has been preceded by repatriation of the corresponding foreign currency, supported by matching banking evidence.

- Dossier Requirement (Art. 5): Banks must open a dedicated prefinancing file before any booking takes place, using a strict naming format (e.g., OMCM SA-10001-PR-001-03-2026).

- Rejection Obligation (Art. 6): Any prefinancing received without proof of prior repatriation must be rejected and the funds returned to the originator.

For Payment Institutions:

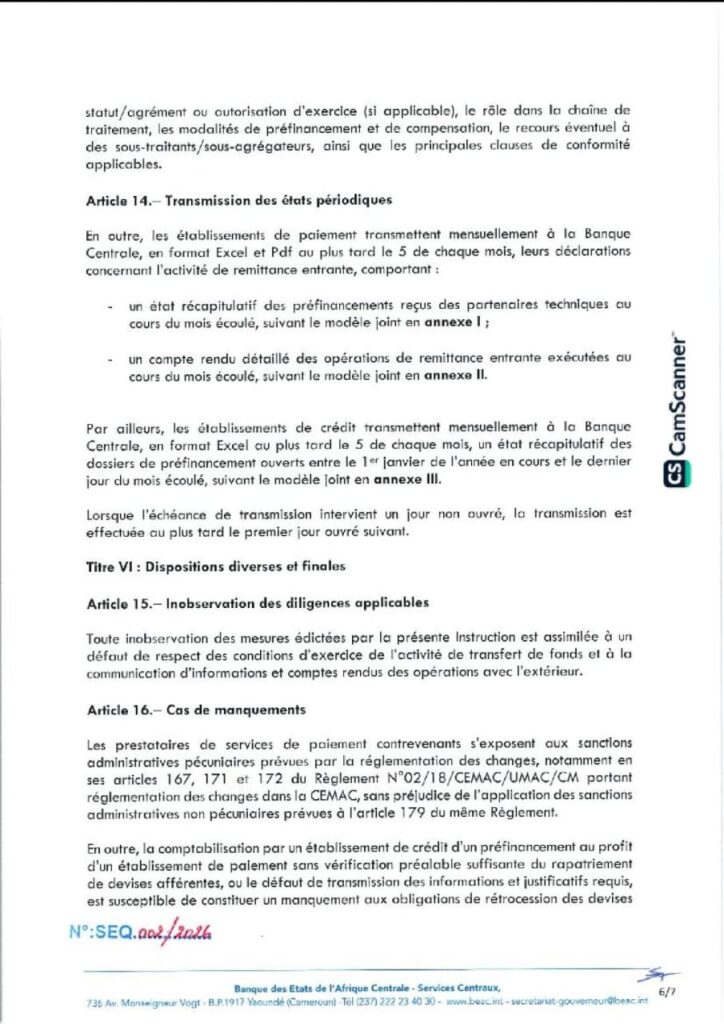

- Reporting of Technical Partners (Art. 13): Within two weeks of publication, all existing technical partner contracts must be submitted to BEAC, including a detailed fact sheet.

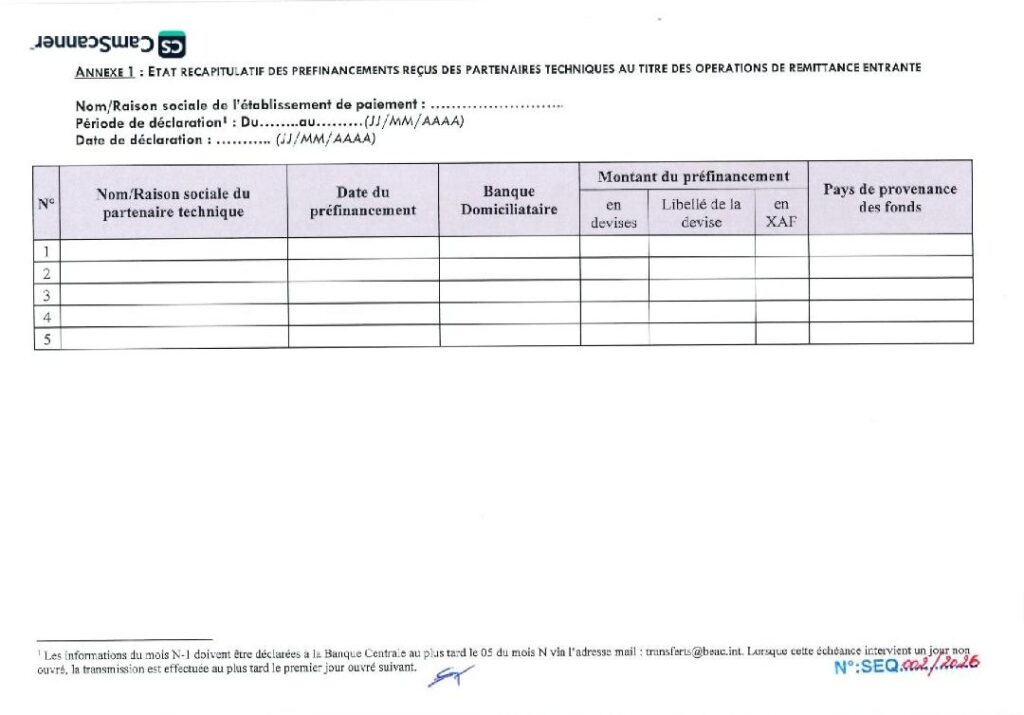

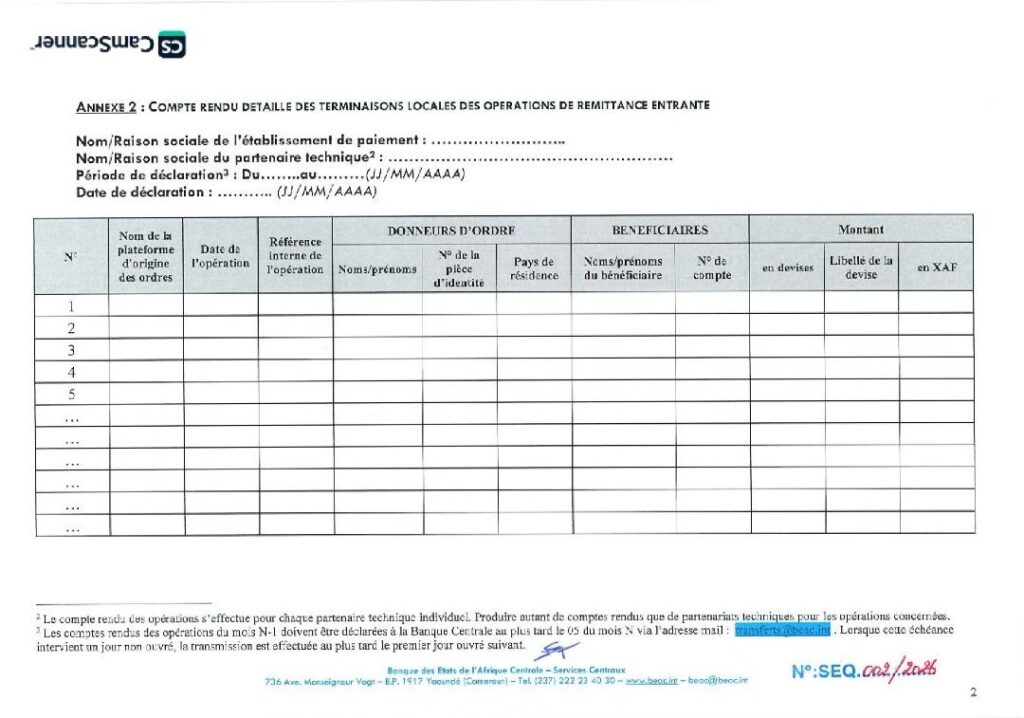

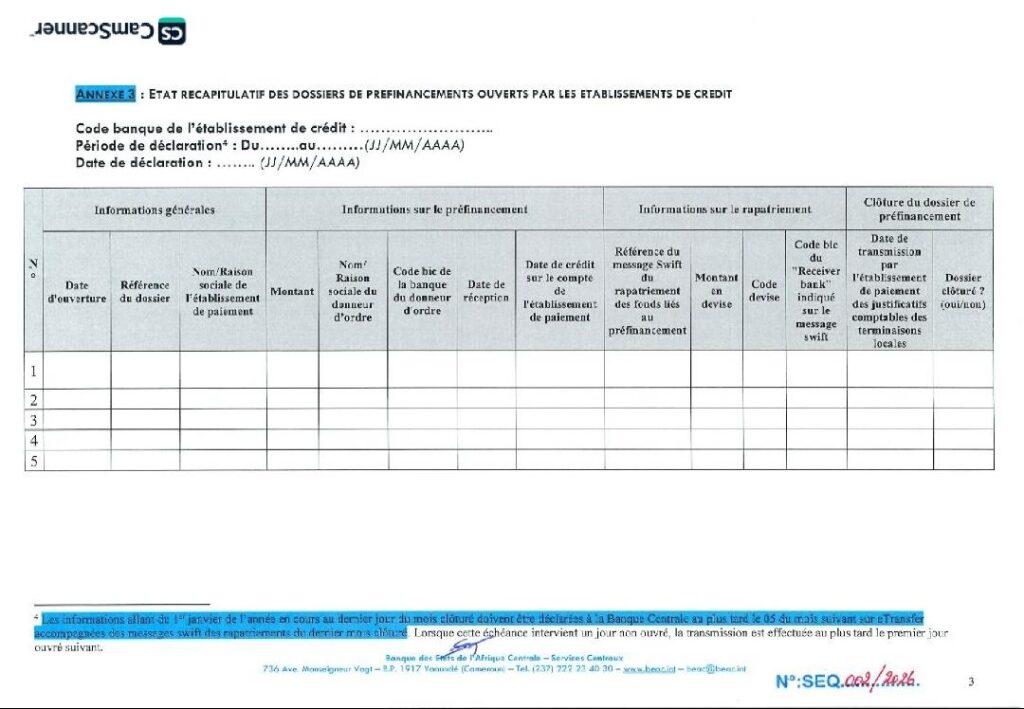

- Monthly Declarations (Art. 14): By the 5th of each month, payment institutions must submit two reports to BEAC (Excel & PDF):

- Annexe I: Summary of prefinancings received.

- Annexe II: Detailed account of local terminations (including sender ID, beneficiary, amounts in foreign currency and XAF).

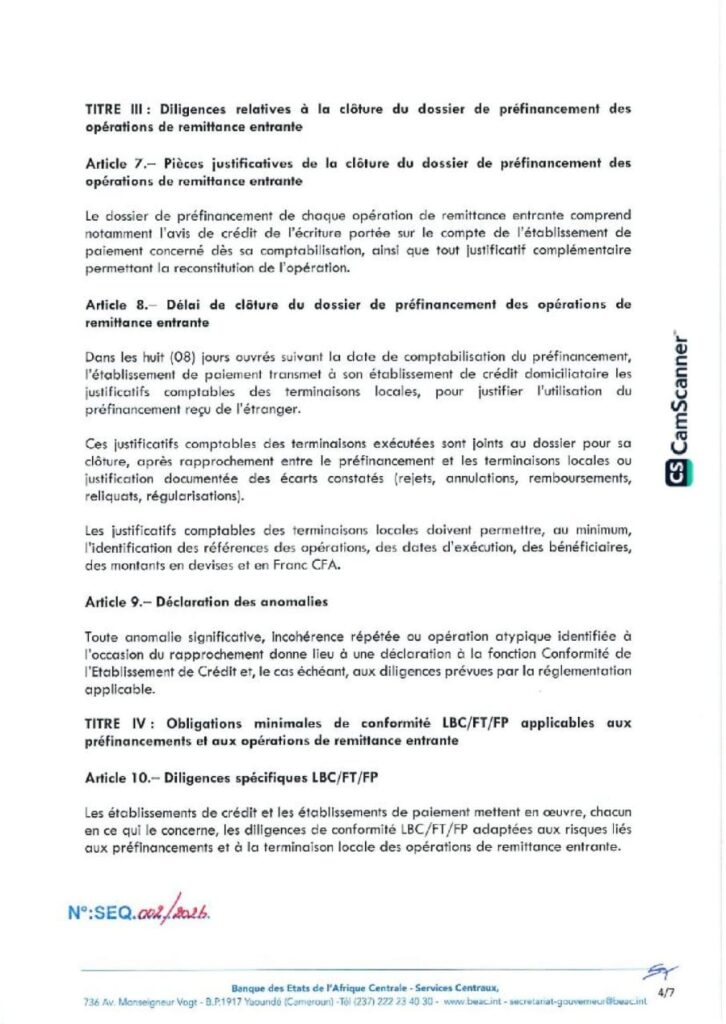

- Closure Deadline (Art. 8): Within eight (8) working days after booking the prefinancing, the payment institution must provide supporting documents of local terminations to its bank to close the dossier.

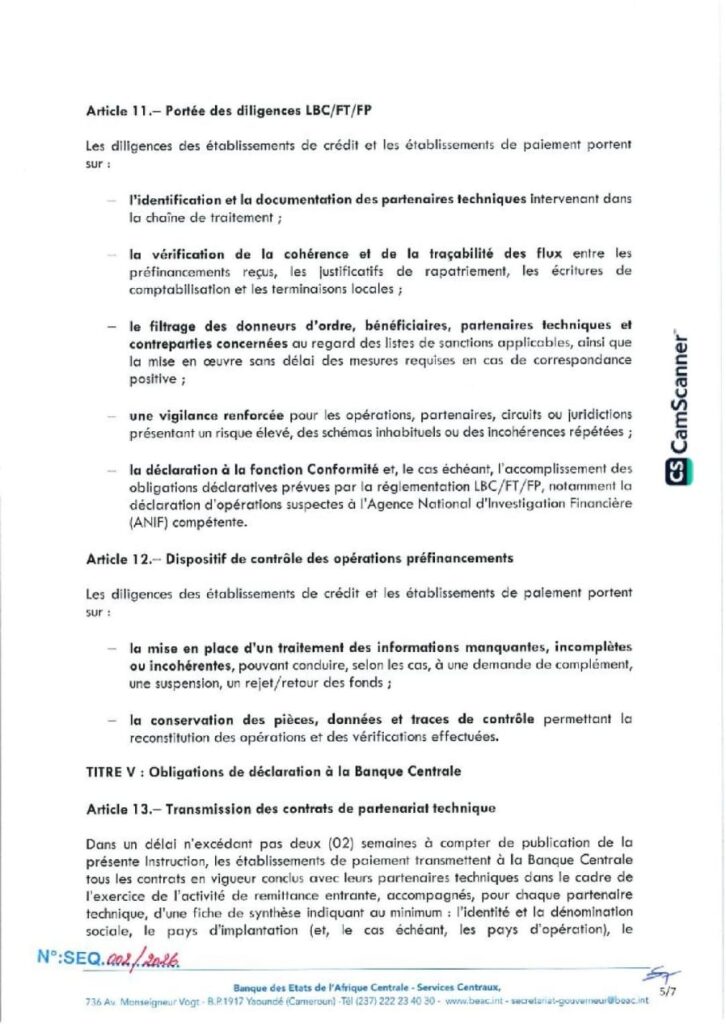

AML/CFT Obligations (Art. 10-12):

Both banks and payment institutions must implement enhanced due diligence on technical partners, screen against sanction lists, and report any anomalies or suspicious transactions to the relevant National Financial Investigation Agency (ANIF).

Sanctions for Non-Compliance

The Instruction explicitly warns that any failure to observe these measures constitutes a breach of the conditions for exercising money transfer activities.

Offenders face:

- Financial administrative sanctions under Articles 167, 171, and 172 of CEMAC Exchange Regulation N°02/18.

- Non-financial administrative sanctions under Article 179 of the same Regulation.

- Banks that credit prefinancing without prior repatriation verification also risk sanctions for breach of currency retrocession obligations under Article 161.

Strategic Implications for the Sector

- End of “Post-Facto” Settlement: The previous practice of settling foreign currency after local payout is effectively prohibited.

- Liquidity Management Pressure: Payment institutions must now ensure their technical partners repatriate FX before funds are credited locally, fundamentally altering float and treasury workflows.

- Bank-PSP Relationship Shift: Banks are now front-line gatekeepers. They must reject non-compliant flows, making correspondent banking due diligence even more critical.

- Data Intensity: Annex II requires granular beneficiary-level data, meaning PSPs must enhance their internal record-keeping and reconciliation engines.

Final Takeaway

BEAC Instruction N°002/GR/2026 is not a technical guideline; it is a binding foreign exchange enforcement tool. For compliance professionals in the CEMAC region, the message is clear: traceability of foreign currency repatriation is now the mandatory precondition for any inbound remittance payout.

The era of invisible prefinancing is over.